Chain transactions – VAT treatment

If the goods are supplied only between two VAT taxpayers, i.e. the seller and the buyer, and the goods are shipped or transported from one EU country to another EU country (or to a non-EU country), the rules for settling VAT are generally simple. As a rule, there is an intra-Community supply of goods (ICS) in the country of dispatch, and an intra-Community acquisition of goods (ICA) in the country of goods’ destination, respectively. And when the destination is an non-EU country there is an export of goods in the country of dispatch and import of goods in the country of the goods’ destination accordingly.

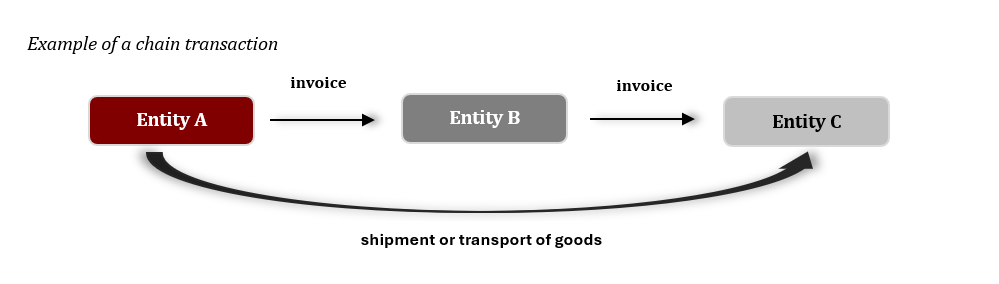

However, the rules for settling VAT on international transactions become more complicated when the same goods are the subject of several supplies, but are actually moved only from the first supplier to the final buyer, i.e. in the case of the so-called “chain transactions”.

The special feature of a chain transaction is that there is only one physical movement of goods and several supplies. Since each of the entities has the right to dispose of the goods as owner, although the entities other than the first and the last do not physically dispose of the purchased goods, each transaction constitutes a supply of goods.

In the case of an international chain transaction, when goods are moved between different countries, the key issue is to determine which delivery should be assigned to the transport of goods. It should be noted that this is critical for determining the place of supply for each supply in the chain, and thus for determining the VAT consequences for each entity in a chain transaction.

If several entities supply the same goods in such a way that the first one delivers the goods directly to the last buyer, and the goods are shipped or transported, the shipment or transport of the goods is assigned to only one supply.

In order to correctly assign the shipment or intra-Community transport to one of the supplies, it is necessary to make an overall assessment of all the circumstances involved to determine which delivery meets all the conditions related to an intra-Community supply (see CJEU judgments C-245/04 and C-430/09).

As a result, in the case of chain transactions, only one supply of goods may constitute a so-called “movable supply” i.e. ICS or export of goods.

In turn, other supplies in the chain constitute so-called “immovable supplies” (i.e. not related to transport) taxed in the country where the dispatch or transport of goods begins (supplies preceding the movable supply) or where this dispatch or transport ends (supplies following the movable supply).

Determining which supply is “movable” is key to assess the VAT consequences for all participants in a chain transaction.

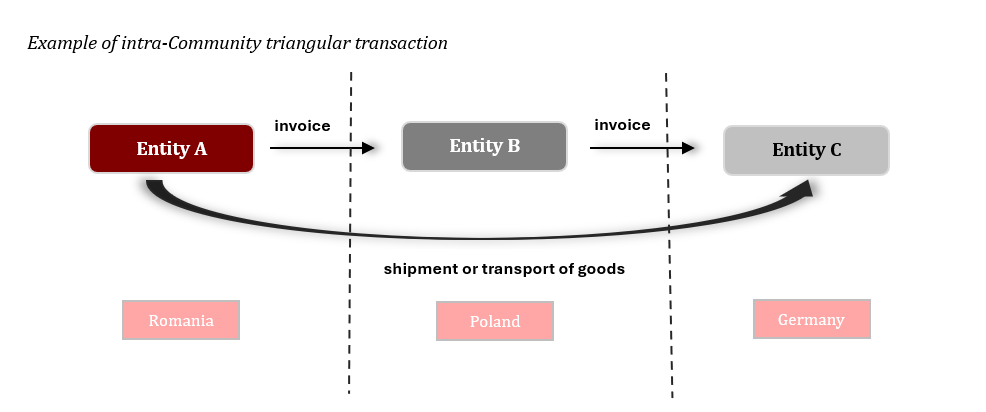

In the case of an intra-Community triangular transactions (“ITT“), in which the first delivery is “movable supply”, it is possible to apply a simplified procedure under certain conditions.

The essence of this procedure is the adoption of a “legal fiction” of taxation of ICA by the second taxpayer, while the actual obligation to settle VAT on the supply of goods made by the second taxpayer in the country where the dispatch or transport of the goods ends, is transferred to the last (third) taxpayer in the ITT.

How can we help?

If you consider taking part in chain transactions when goods are shipped or transported from or to Poland let us know as we will be happy to provide you with our tax advisory support in this matter.